Welcome to your weekly macro roundup. This comprehensive edition covers the United States, Europe, and key emerging markets with in-depth analysis of the week's most significant economic developments and what they mean for markets ahead.

🇺🇸 May's 172K payrolls and 54.0 ISM demolished the tariff recession call

May nonfarm payrolls printed 172,000 against an 80,000 consensus, and ISM Manufacturing PMI hit 54.0, a four-year high. Two data points that demolished the tariff recession call and left the Fed sitting on its hands.

🇪🇺 ECB walks into June hike as services PMI contracts and energy inflation hits 10.9%

Composite PMI fell to an 18-month low of 48.5 in May as energy-driven inflation hit 3.2%, pushing the ECB toward a June 11 rate hike into a shrinking services economy. September is the real decision, and the ECB has historically struggled to make it.

🇬🇧 BoE's Greene relitigates the transitory debate as services PMI tips into contraction

MPC member Megan Greene signalled a possible rate hike within months, warning energy pass-through will push CPI back toward 3.3% in Q3. April CPI fell to 2.8%; services PMI contracted to 49.3 in May. June 17 is the test.

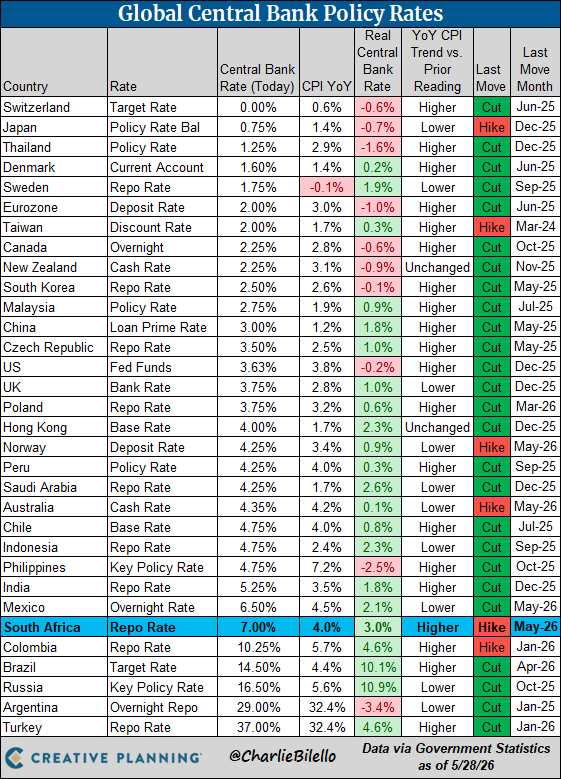

🌏 Indonesia doubled the expected rate hike, and the rupiah broke to a record 18,000 anyway

Bank Indonesia's 50 basis point hike to 5.25% couldn't arrest the rupiah, which broke through 18,000 per dollar for the first time on record. An $18bn Q1 2026 balance-of-payments reversal shows the structural vulnerability that rate policy alone can't fix.

🇨🇳 China's PMI divergence looks manageable; what's happening to producer margins does not

China's official PMI flatlined at 50.0 in May while the Caixin gauge held at 51.8, but April PPI surged to +2.8% year-on-year, a 45-month high. Manufacturers are eating the cost shock, not passing it through.

That wraps up this week's macro roundup. We'll be back with daily updates throughout the week and another comprehensive weekly edition next time. If you know someone who would appreciate this analysis, feel free to share. More signal, less noise, as ever. Cheers.

Discussion