Good morning, macro enthusiasts. Here's your daily roundup covering the United States, Europe, and key emerging markets. We cut through the noise to deliver the essential facts, key surprises, and meaningful context from each region in one place.

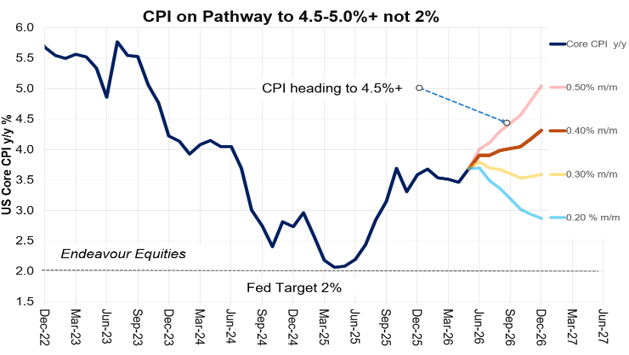

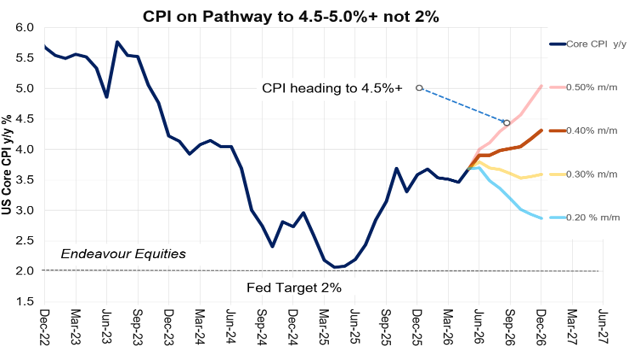

🇺🇸 Williams' 0.2% inflation line is already broken, and CPI lands tomorrow

New York Fed President John Williams set a 0.2% monthly core inflation threshold for holding rates, but core PCE has averaged 0.34% in 2026. June CPI and PPI data land July 14-15, two weeks before the Fed's July 28-29 meeting.

🇪🇺 France pays a growing premium over Germany, even in three-month bills

French borrowing costs are now running above Germany's even in three-month bills, with the 10-year OAT-Bund spread near 70 basis points as investors price in a fiscal risk premium ahead of Thursday's eurozone inflation data.

🇬🇧 The BoE's own chief economist is now its loudest hawk

Huw Pill, the BoE's chief economist, dissented for a rate hike in June alongside Megan Greene. He speaks today with retail sales up 3.1% year-over-year and inflation at 2.8%, two weeks before the July 30 rate decision.

🌏 India's inflation breaks back above target just as Hormuz sends oil higher

India's June CPI hit 4.38%, breaching the Reserve Bank of India's 4% target for the first time since January 2025, as Brent crude jumped past $79 a barrel on Strait of Hormuz fighting. Brazil's central bank held its 2026 rate forecast at 14.00%, suggesting its own easing cycle has stalled too.

🇨🇳 China's AI export boom masks a consumer economy that's still shrinking

China's manufacturing PMI beat forecasts at 50.3 on AI-linked exports, but June retail sales are forecast to shrink roughly 1% as Q2 GDP cools to about 4.6%. Thursday's trade data and Friday's GDP release will show how much of Beijing's growth target now rests on exports alone.

That's your daily macro roundup. For more detailed regional deep dives, check out our weekly editions. If you found this useful, feel free to forward it along. More signal, less noise, as ever. Cheers.

Discussion