Welcome to your weekly macro roundup. This comprehensive edition covers the United States, Europe, and key emerging markets with in-depth analysis of the week's most significant economic developments and what they mean for markets ahead.

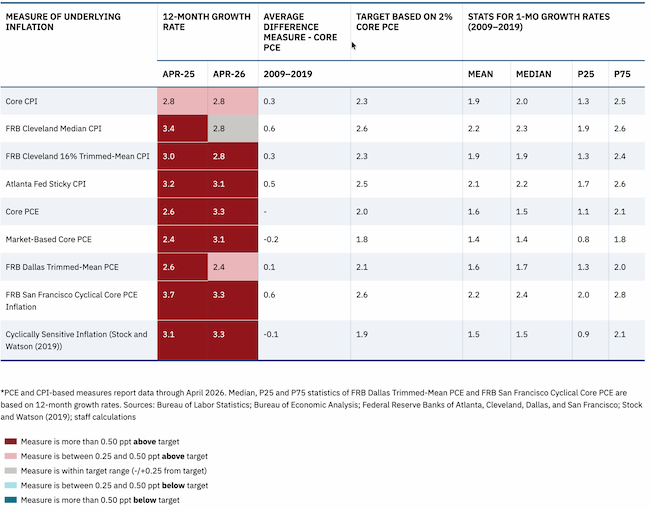

🇺🇸 Yields retreated. The inflation pipeline did not.

Trade services PPI surged a record +2.7% MoM in April while the 10-year Treasury yield fell 24 basis points on ceasefire hopes. Core PCE rose to 3.3% YoY and three FOMC hawks formally dissented, flagging hike optionality the market has not priced.

🇪🇺 Germany's May CPI misses by 30 basis points, and the energy impulse behind Schnabel's post-June case is already fading

Germany's May preliminary CPI printed 2.6%, 30 basis points below consensus, as the energy component slowed to 6.6% from 10.1%. June is locked in; the question is whether the energy impulse Schnabel needs to justify September is already fading.

🇬🇧 UK composite PMI fell to a 13-month low in May while services input costs hit an all-time survey high

UK composite PMI fell to 48.5 in May while services input costs hit an all-time high in the S&P Global survey. The Bank of England's June 18 Monetary Policy Committee meeting is live, not the cut that gilts are pricing.

🌏 EM central banks are fracturing along the current account fault line

Turkey held at 37% but JPMorgan sees a hike to the 40% corridor ceiling as imminent. Mexico's floor sits at 6.50%, where peso stability has more sway than the domestic cycle. Brazil's near-10% real rate on the Selic stands apart from both.

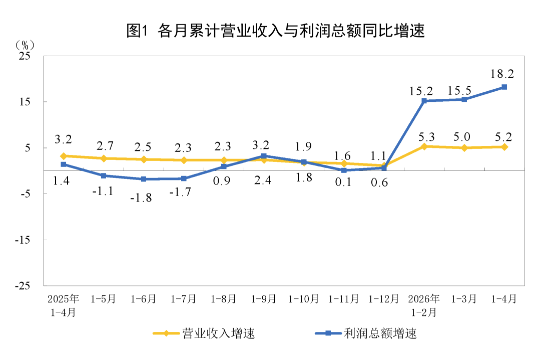

🇨🇳 China's industrial profits are at a 30-month high. Retail sales are at a 40-month low.

China's April industrial profits rose 24.7% year on year, the fastest pace in 30 months, while retail sales grew just 0.2%, a 40-month low. High-tech FDI was up 20.3% even as total inflows fell 10.3%.

That wraps up this week's macro roundup. We'll be back with daily updates throughout the week and another comprehensive weekly edition next time. If you know someone who would appreciate this analysis, feel free to share. More signal, less noise, as ever. Cheers.

Discussion