Welcome to your weekly macro roundup. This comprehensive edition covers the United States, Europe, and key emerging markets with in-depth analysis of the week's most significant economic developments and what they mean for markets ahead.

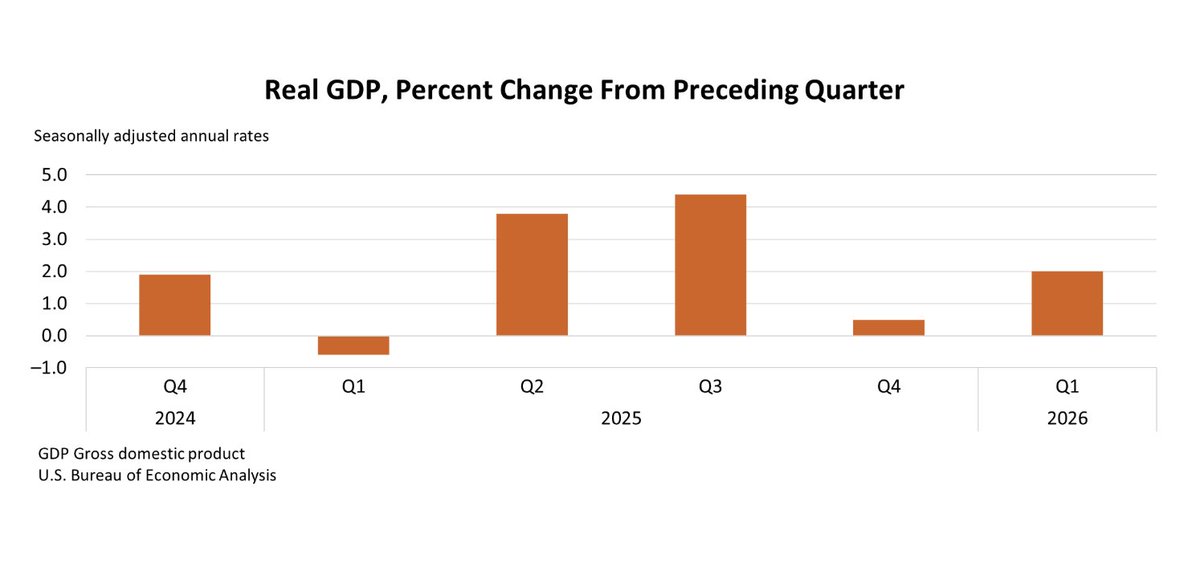

[US] Q1 GDP Climbs to 2.0% But a 4.5% PCE Deflator Traps the Fed in an Extended Hold

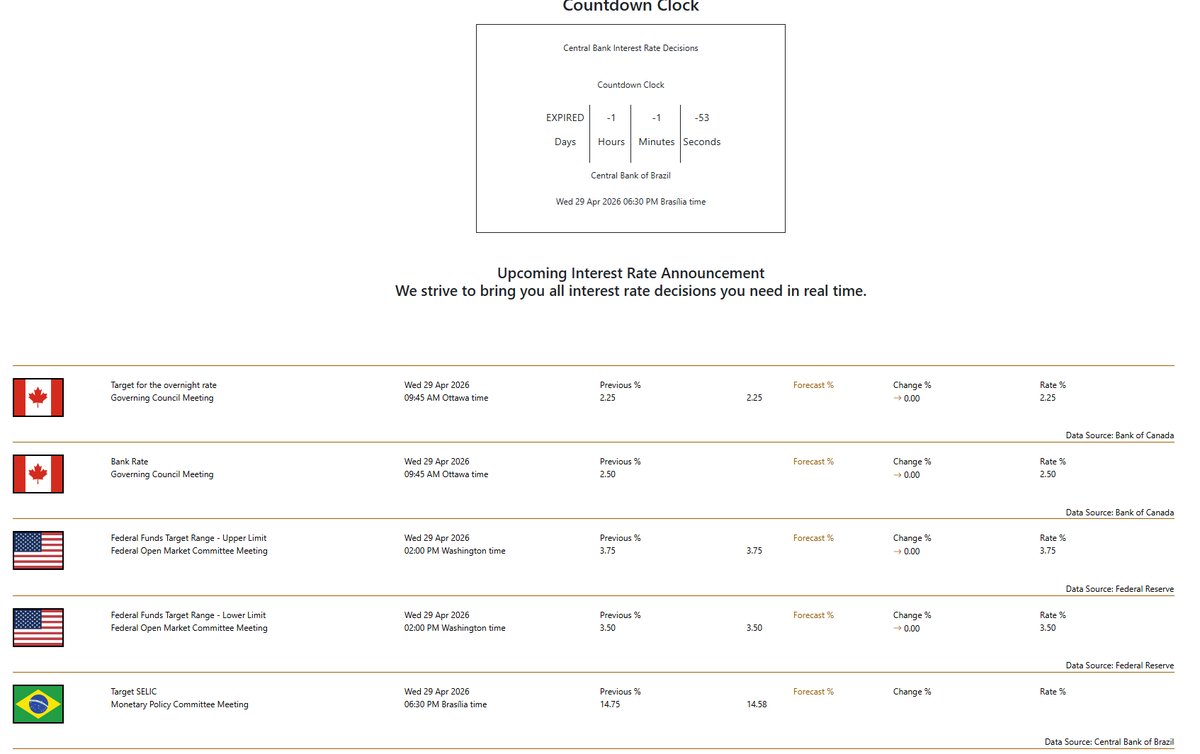

US Q1 GDP rebounded to 2.0% but a 4.5% PCE deflator and 3.4% YoY wage growth locked the Fed into an extended hold at 3.50-3.75% on April 29. Initial jobless claims at 189,000 show no labor market softening in sight.

[EU] ECB Cornered: Inflation Re-Accelerates to 3.0% as Q1 Growth Stalls at 0.1%, Closing Every Policy Exit

Eurozone HICP surged to 3.0% YoY in April from 2.6%, while Q1 GDP grew just 0.1% QoQ, leaving the ECB holding at 2.0% with real rates at -1.0% and no clear path to cut or hike.

BoE's 8-1 Hold Masks a 2.6-Point Inflation Uncertainty Range That Tests State-Contingent Policy

BoE held Bank Rate at 3.75% in an 8-1 vote, with Chief Economist Huw Pill dissenting for a hike. The April MPR projects CPI peaking between 3.6% and 6.2%, a 2.6-point range reflecting uncertainty over Middle East energy pass-through.

[EM] Mexico's Worst Post-COVID Quarter Exposes the Tariff Trap in the Nearshoring Trade

Mexico's economy contracted -0.8% q/q in Q1 2026 (-3.16% SAAR), its worst non-pandemic quarter in recent memory, as US tariff uncertainty derails the nearshoring trade. Brazil, Indonesia, and India illustrate three diverging EM responses to Washington's policy whipsaw.

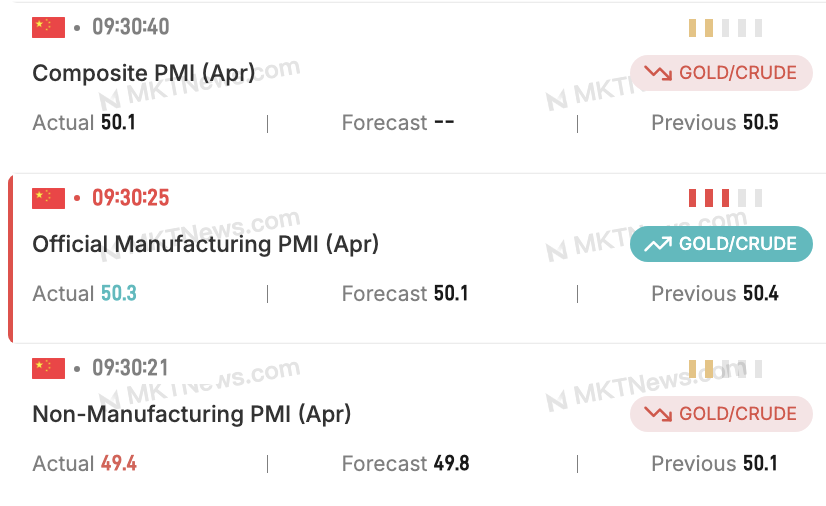

[CN] China's April PMI: Caixin at a five-year high, services in contraction

Caixin manufacturing PMI hit a five-year high of 52.2 in April; non-manufacturing fell to 49.4. The factory sector is outperforming. Services are not.

That wraps up this week's macro roundup. We'll be back with daily updates throughout the week and another comprehensive weekly edition next time. If you know someone who would appreciate this analysis, feel free to share. More signal, less noise, as ever. Cheers.

Discussion