Good morning, macro enthusiasts. Here's your daily roundup covering the United States, Europe, and key emerging markets. We cut through the noise to deliver the essential facts, key surprises, and meaningful context from each region in one place.

🇺🇸 ISM prices paid hit a four-year high as markets price June's hold but not its signal

ISM manufacturing prices paid hit 85.3 in May, the highest since early 2022, completing a three-month, 7-point acceleration. Markets have June 17 resolved. The dot plot and dissent vote under Kevin Warsh may read it differently.

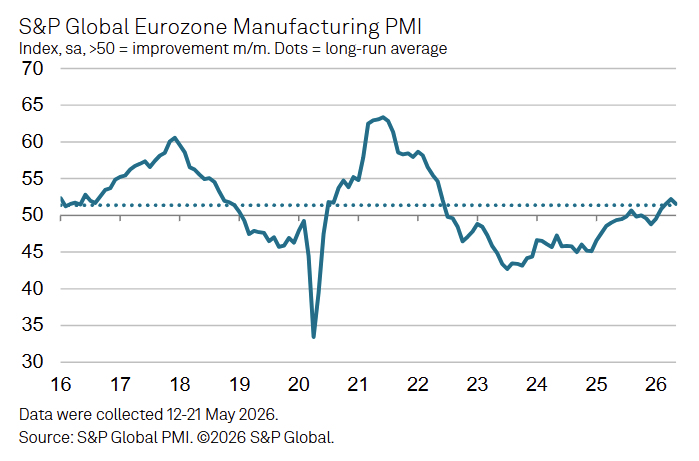

🇪🇺 ECB's June hike is priced; the May PMIs just complicated the second one

Eurozone Manufacturing PMI printed 51.6 in May, with France back in contraction at 49.7 and input costs at a four-year high. A June ECB hike is 91% priced; the supply-side cost picture makes a second move in September harder to defend.

🇬🇧 UK's April CPI miss is an Ofgem artefact; the Q3 spike is already on the calendar

April CPI at 2.8% is 50 basis points below forecast, but the Ofgem cap reset fires 1 July at +13%. The Q3 CPI spike is already locked in, and Bank of England cut pricing built on the April miss is exposed.

That's your daily macro roundup. For more detailed regional deep dives, check out our weekly editions. If you found this useful, feel free to forward it along. More signal, less noise, as ever. Cheers.

Discussion