Good morning, macro enthusiasts. Here's your daily roundup covering the United States, Europe, and key emerging markets. We cut through the noise to deliver the essential facts, key surprises, and meaningful context from each region in one place.

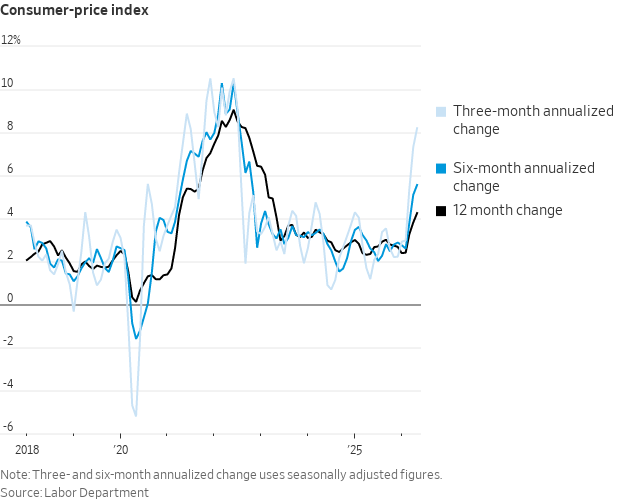

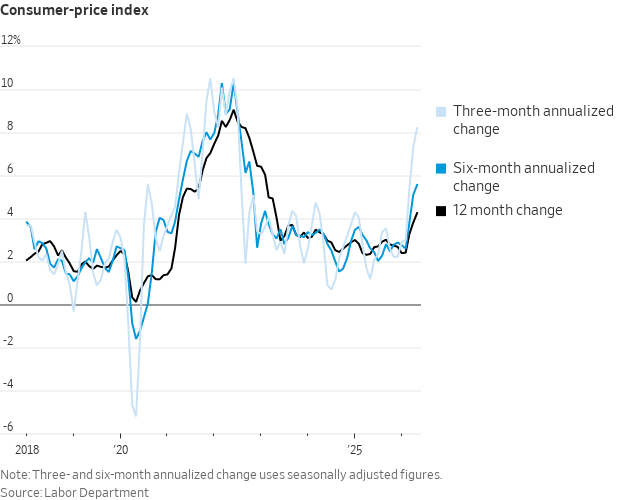

🇺🇸 The energy shock that pushed May CPI to 4.2% may be quietly doing the Fed's work

US May CPI hit 4.2% year-on-year, the highest since mid-2023, as energy prices surged. Core eased to 2.9% and supercore services decelerated sharply. The energy shock is inadvertently doing the Fed's demand-destruction work.

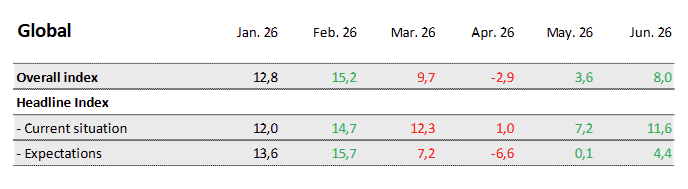

🇪🇺 Germany stays frozen as the ECB prepares to hike, putting tomorrow's staff projections on trial

Sentix eurozone confidence improved to −13.4 in June (forecast: −14.6), but Germany's current conditions sub-index held near crisis lows at −42.5. The ECB meets 11 June; updated staff projections carry all the forward guidance weight for September.

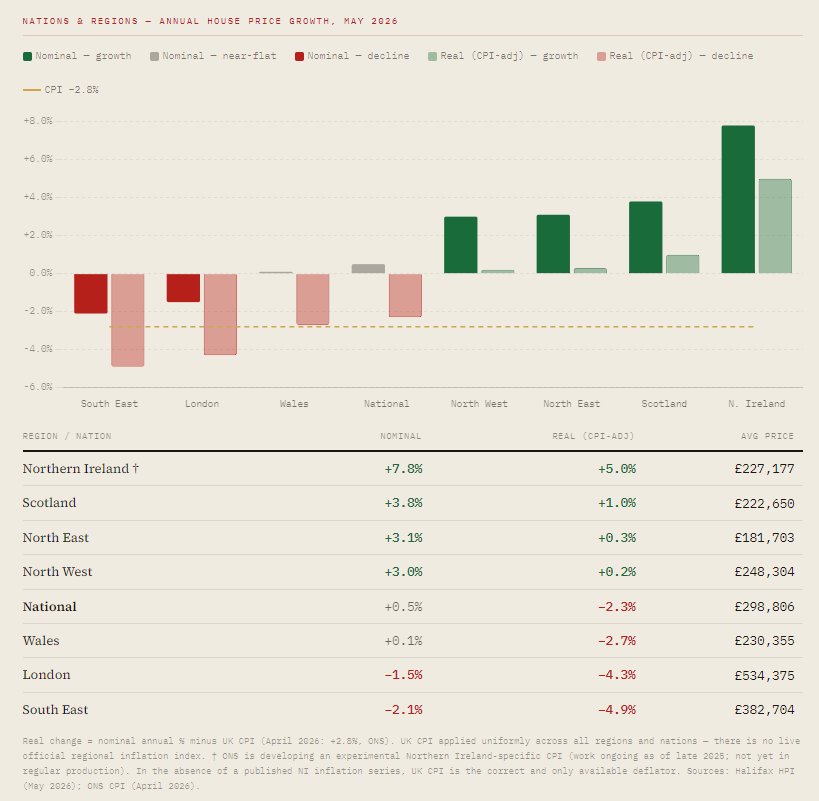

🇬🇧 BoE gets 24 hours between May CPI and its rate decision, with the July energy reset already locked in

The MPC votes June 18. May CPI lands June 17. With Ofgem's +13% energy cap reset locked in for July 2026, a CPI upside surprise would force the 2-year gilt to reprice the cut probability in a single overnight session.

🌏 EM easing cycles are hitting their inflation ceilings, and Brazil's Copom is up first

India's RBI held at 5.25% but lifted its FY2027 CPI forecast to 5.1%. Brazil's Copom meets June 16-17 as the first test of whether EM easing cycles can survive domestic inflation that keeps running above target.

🇨🇳 China's record surplus masks a factory-gate squeeze that is ending two years of cheap-goods disinflation

May PPI rose +3.9% year on year, fastest since July 2022, against CPI at +1.2%; the factory-gate spread is 2.7 points and the cheap-goods disinflation era looks to be ending. Trade surplus: $105.43bn against the $92.1bn forecast.

That's your daily macro roundup. For more detailed regional deep dives, check out our weekly editions. If you found this useful, feel free to forward it along. More signal, less noise, as ever. Cheers.

Discussion