Good morning, macro enthusiasts. Here's your daily roundup covering the United States, Europe, and key emerging markets. We cut through the noise to deliver the essential facts, key surprises, and meaningful context from each region in one place.

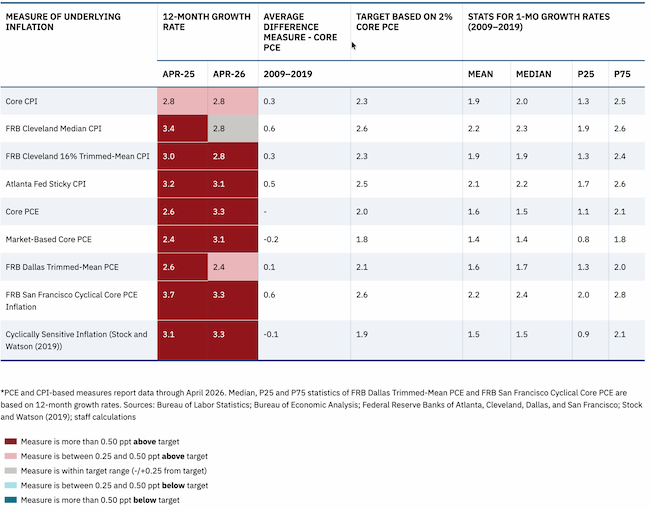

🇺🇸 Core PCE missed on the month, rose on the year, and the yield bid has a 60-day sponsor

Core PCE rose 0.2% in April, missing the 0.3% consensus, but the annual rate climbed to 3.3%, its highest since late 2023. St. Louis Fed President Musalem flagged a possible rate hike; the 10-year yield's relief rally rests partly on a 60-day Iran ceasefire.

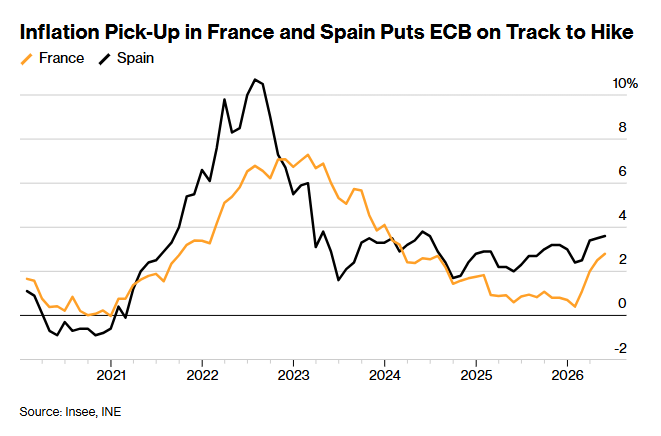

🇪🇺 France contracted in Q1, German energy import costs jumped 31.0%, and money markets still have the ECB hiking on June 11

France's economy shrank −0.1% in Q1 and German energy import prices jumped +31.0% year on year in April. The ECB's June 11 rate decision is far more contested than money market pricing suggests.

🇬🇧 Bailey anchors a hold before June's services CPI test

Bailey's Reykjavik remarks were conditional, not dovish. UK services CPI fell to 3.2% in April, but a re-acceleration toward 4%-plus in the May release lands the same week as the June 18 Monetary Policy Committee decision.

🌏 SARB's 4-2 hike leaves the harder question to May CPI

SARB hiked to 7.00% in a 4-2 vote. The majority cited M3 at 9.82% and credit extension at 9.20% year-on-year; the doves read the 90-basis-point CPI jump as a fuel reversal and held. May CPI settles the argument.

🇨🇳 PBOC's May easing has reached the offshore channel, but the order book hasn't followed

Hong Kong's April M3 money supply jumped to 3.1% year-on-year from 1.2%. PBOC's May stimulus has reached the offshore channel. China's May NBS Manufacturing PMI, due imminently, will show whether it has reached real demand at all.

That's your daily macro roundup. For more detailed regional deep dives, check out our weekly editions. If you found this useful, feel free to forward it along. More signal, less noise, as ever. Cheers.

Discussion